What You’ll Learn

How to understand your Closing Disclosure form

Why your Closing Disclosure may vary from your Loan Estimate

The significance of different dates on your Closing Disclosure

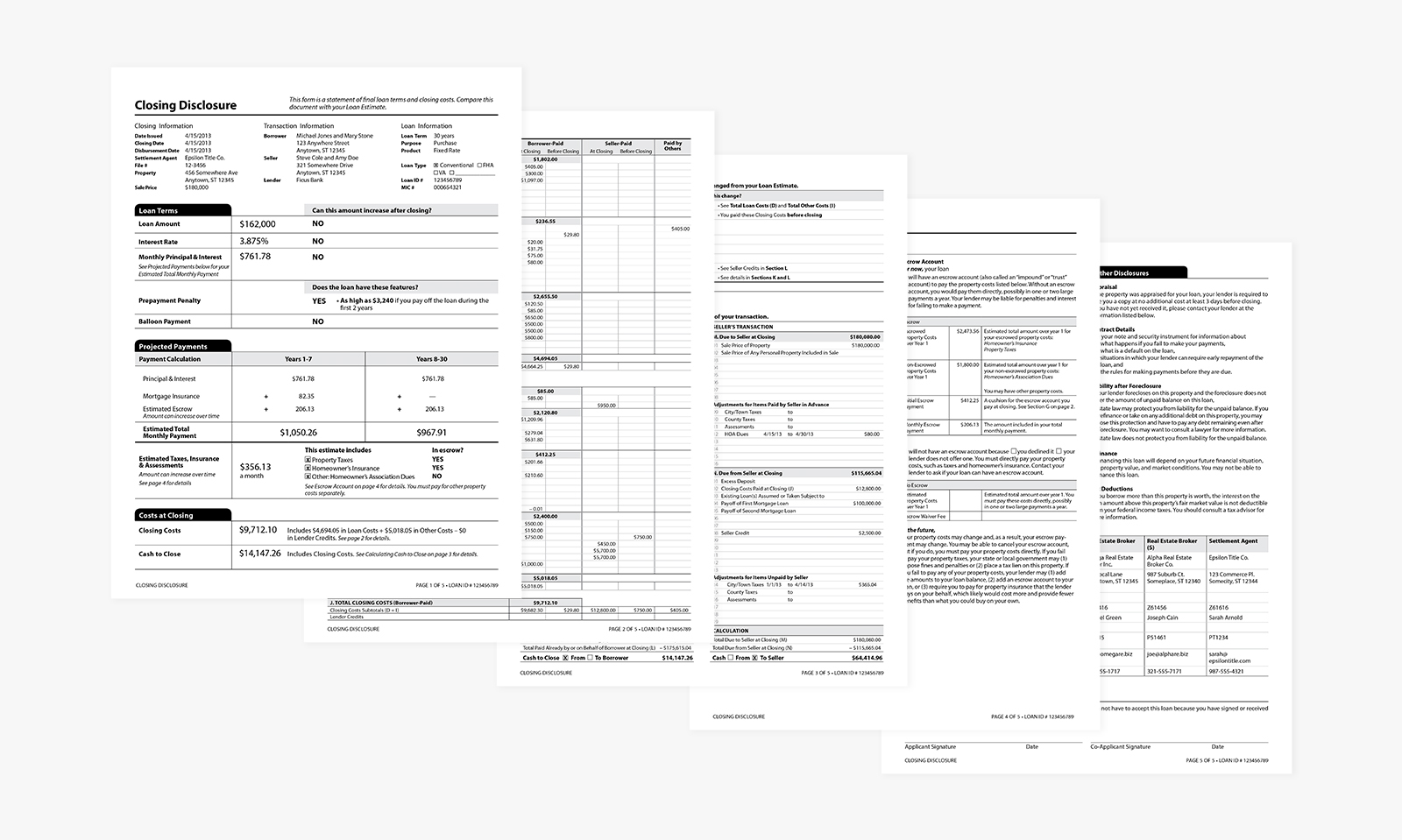

A Closing Disclosure is a five to six-page form that provides final details about the mortgage loan you have selected, including the loan terms, your projected monthly payments, and how much you will pay in fees and other costs to get your mortgage (closing costs).

Mortgage lenders are required to provide the initial Closing Disclosure at least three business days before you close on your loan, giving you time to compare your final terms and costs to those estimated in the Loan Estimate you had previously received.

That three days also give you time to ask any questions before you go to the closing table.

You should receive your initial Closing Disclosure, any revised Closing Disclosures (if necessary), and your final Closing Disclosure, which you will sign on paper on the day of closing.

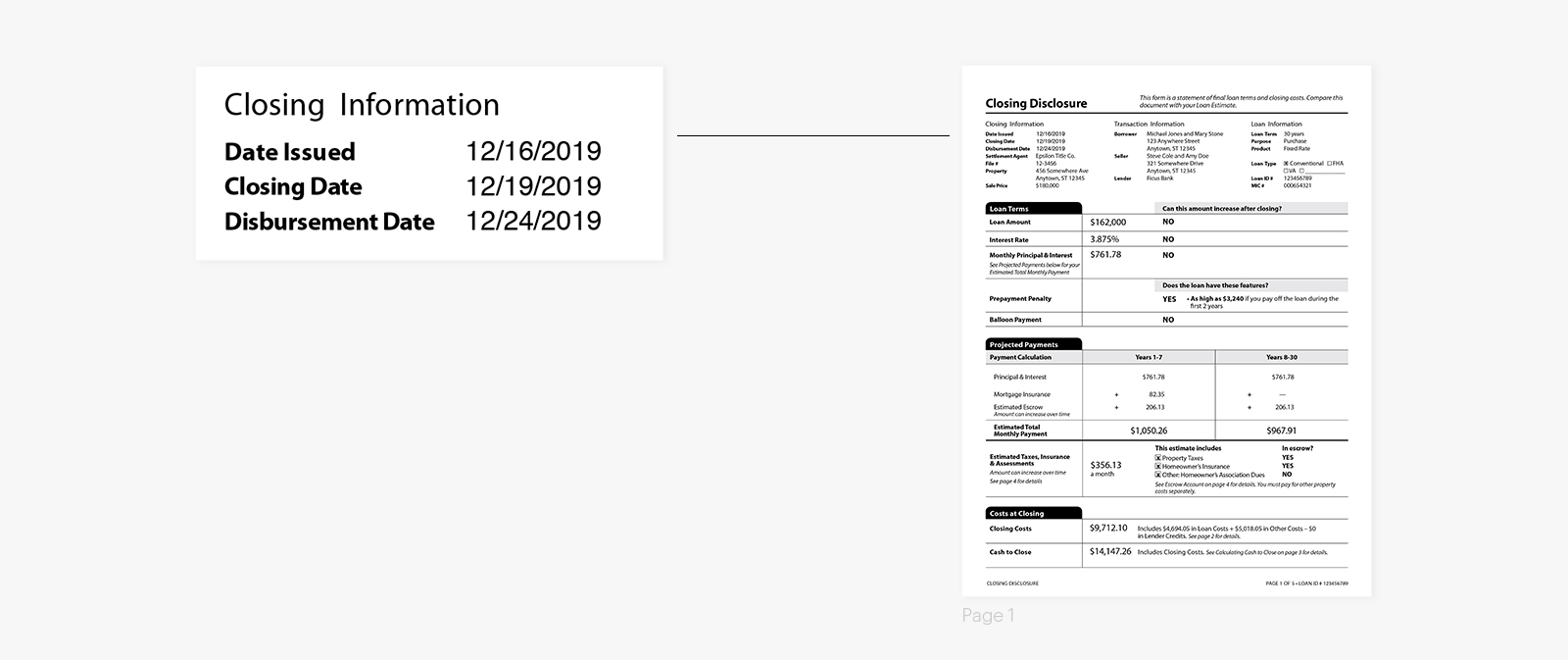

There are three important dates reflected in the top left corner of your initial Closing Disclosure:

Date issued: the date the initial Closing Disclosure was provided to you. For the purposes of the closing date, we assume you will acknowledge receipt of the initial Closing Disclosure the same day it was provided to you.

Closing date: if you’re refinancing an existing mortgage, we assume you will close three business days after you’ve acknowledged receipt of the initial Closing Disclosure.

If you’re purchasing a new home, the closing date will reflect your “Close of Escrow” date (if the state you’re purchasing in requires closing and disbursement to occur on the same day).

If you’re purchasing a new home in a state that allows you to close prior to your “Close of Escrow” date, then the closing date on your initial Closing Disclosure will reflect your earliest possible signing date.

Disbursement date: the date your loan will fund, which is generally the same day the title company will “disburse” your transaction (to be recorded with the county, pay off any existing liens, pay third parties, initiate any cashback you’re receiving, etc.). If you’re refinancing the existing mortgage on your primary residence, then the disbursement date will reflect the first business day after your three-day “right of rescission” has passed. The disbursement date is also the date prepaid interest starts accruing on your new mortgage (see section F of your Closing Disclosure).

Click here to read the original post by Better Mortgage.

Blumberg Offers a Variety of Real estate Related Forms

Condominium lease and sale forms

Real estate practice: contracts of sale for residential, multi-family, office, commercial, land; loan contract

Co-operative apartment lease and sale forms

Deeds, warranty, covenant, quitclaim, etc.

Foreclosure proceedings

Property condition disclosure statement

Click for a full list of Real Estate related forms by Blumberg.